There was a time when upgrading from the OCR to CCR felt like going from a 3-star hotel to The Ritz. The jump in price per square foot (psf) — often over $1,000 — kept even aspirational homeowners grounded.

But something flipped.

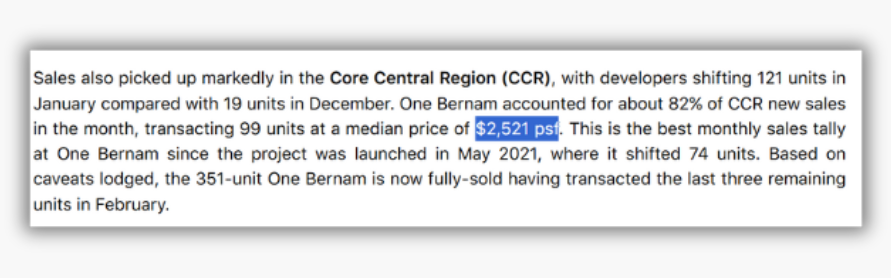

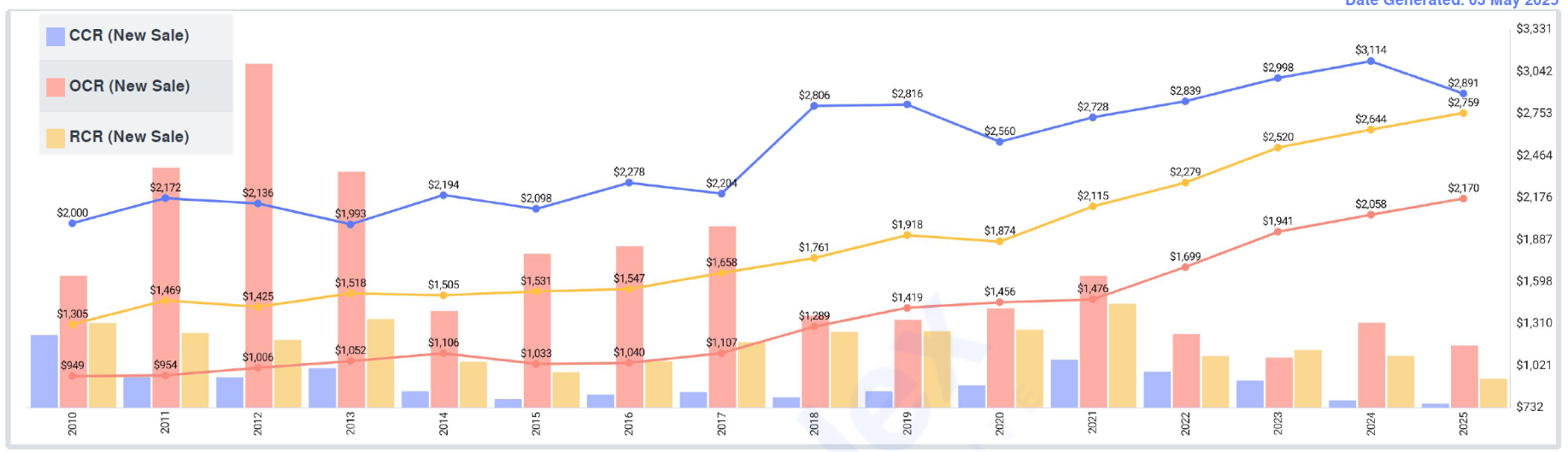

In Q1 2025, URA data revealed a rare pricing distortion:

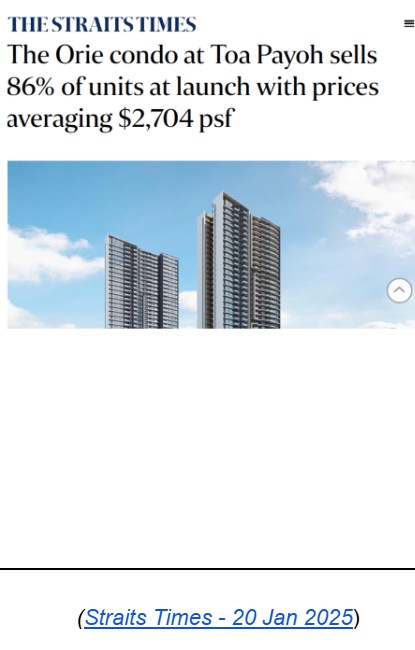

Now compare that to launch prices outside the core:

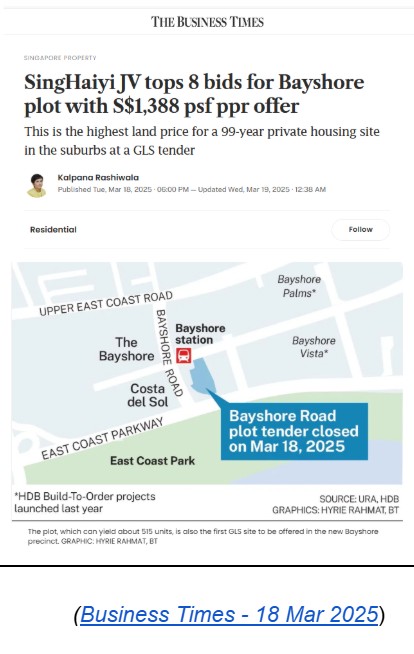

The Bayshore GLS indicates future OCR launches pushing ~$3,000 psf, aligning closely with CCR resale prices—closing the affordability gap to the narrowest seen in 15 years.

This isn’t a temporary anomaly—it’s a new reality.

New OCR launches are now priced within 5–10% of resale units in the CCR.

What if the OCR’s future peak is already today’s CCR floor?

(Propnex.com – 17 Feb 2025)

When the cost of mass-market becomes indistinguishable from prime, the upgrade ladder breaks.

What replaces it is a convergence — and that should concern every buyer who still assumes the CCR is out of reach.

This shift wasn’t accidental. It was decades in the making — powered by decentralisation, income growth, and product reform.

Now, for the first time in years, the CCR has become relatively affordable — simply because everything else caught up.

The common view was that the CCR didn’t move because it was too expensive.

But that’s not entirely true.

For much of the past decade, the real problem was design — not price.

Buyers didn’t walk away because they couldn’t afford it.

They walked away because it didn’t feel like home.

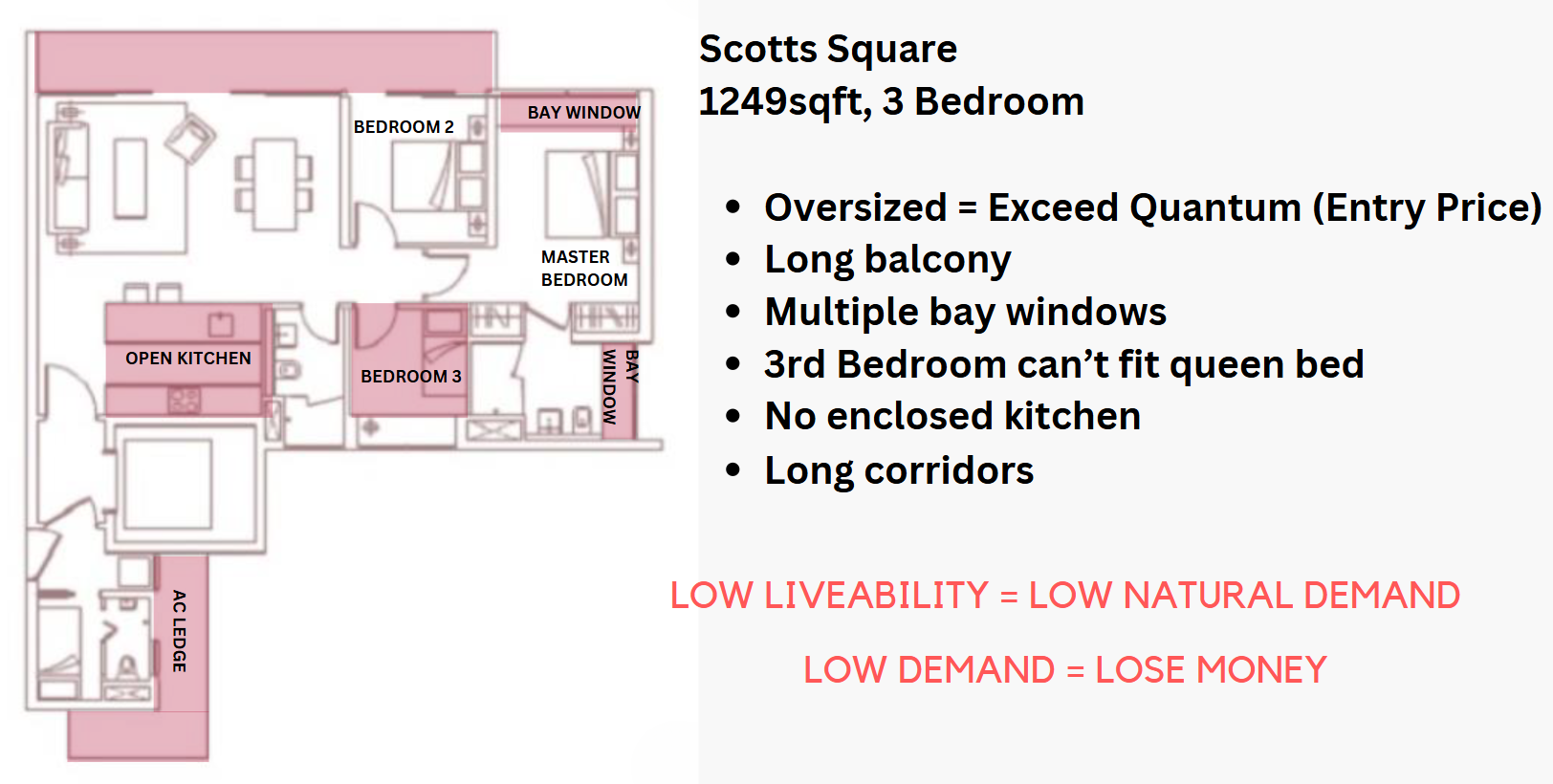

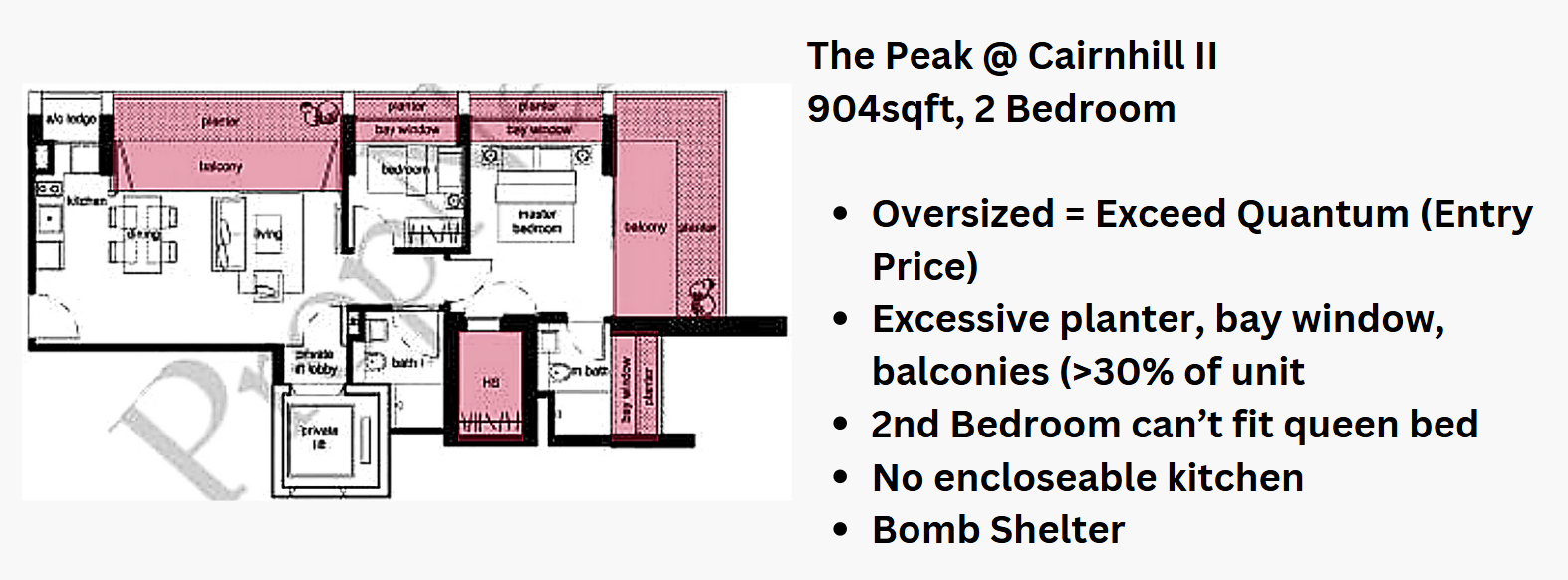

It wasn’t just CCR. Sky Habitat in the RCR — despite its striking architecture — suffered from similar issues.

The result? Poor resale performance, even in desirable locations.

But the product has since been fixed — systematically.

Major URA interventions:

| Date | URA Policy Title | URL |

| 18/10/2022 | Guidelines on Dwelling Units in Non-Landed Residential Developments | URA Circular dc22-10 |

| 01/09/2022 | Harmonisation of Floor Area Definition By URA, SLA, BCA, & SCDF | URA Circular dc22-09 |

| 05/07/2022 | Land Betterment Charge Arising From Planning Applications And/Or Involving Lifting of Restrictive Covenants | URA Circular dc22-08 |

| 17/10/2018 | Bonus Gross Floor Area Scheme for Indoor Recreation Spaces in Private Non-Landed Residential Development | URA Circular dc18-08 |

| 17/10/2018 | Revision to the Balcony Incentive Scheme for Private Non-Landed Residential Developments | URA Circular dc18-07 |

| 28/08/2014 | Retail Guidelines to enhance shoppers’ experience in retail developments and the retail component of mixed-use developments | Retail Guidelines |

| 28/02/2014 | Revision GFA Guidelines Covering Private Outdoor Spaces (PES/PRT) within Non-Landed Strata-Titled Residential Developments | PES Guidelines |

| 27/03/2013 | Guidelines on Retail Unit Size and Corridor Width | URA Circular dc13-02 |

| 07/07/2008 | Changes to GFA Exemptions Guidelines – Bay Windows in all Developments and Planter Boxes within a residential unit | URA Circular d08-17 |

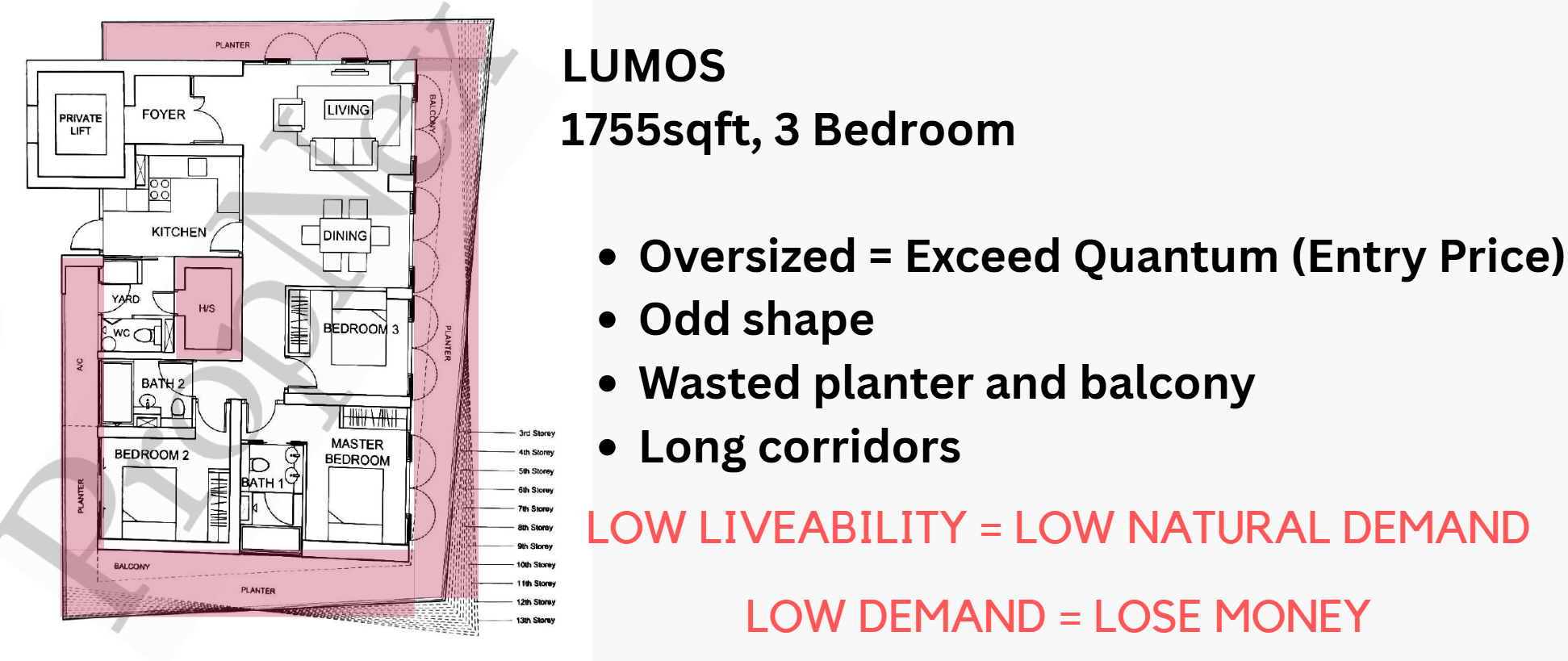

These weren’t cosmetic adjustments — they reshaped the core of residential design.

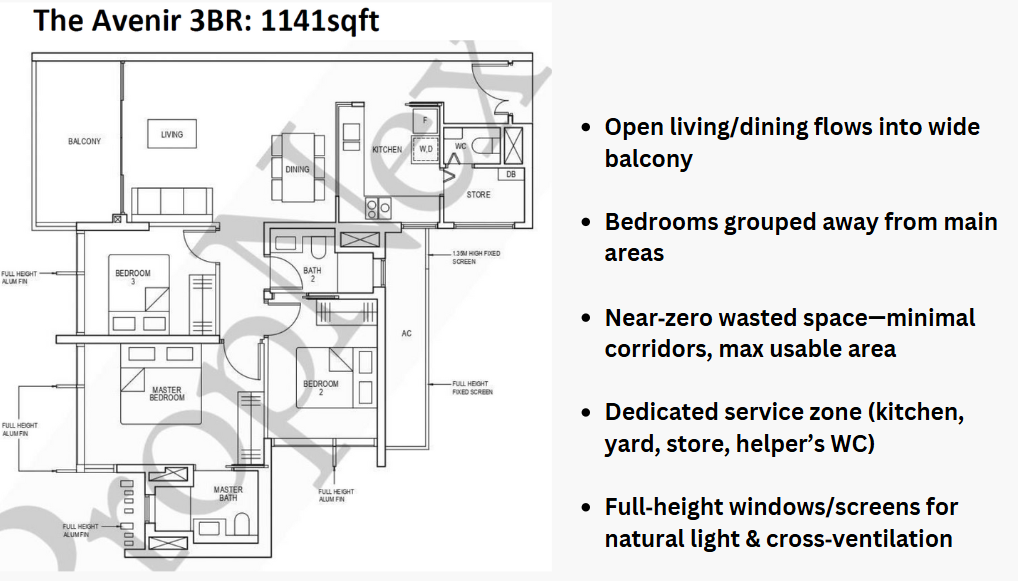

Today, new CCR launches like Irwell Hill Residences, Gramercy Park and The Avenir are built for real living:

When space is wasted, demand disappears — and so do profits.

When space is liveable, value follows.

This is the quiet reset many have missed. And it’s now priced into the new wave of CCR offerings.

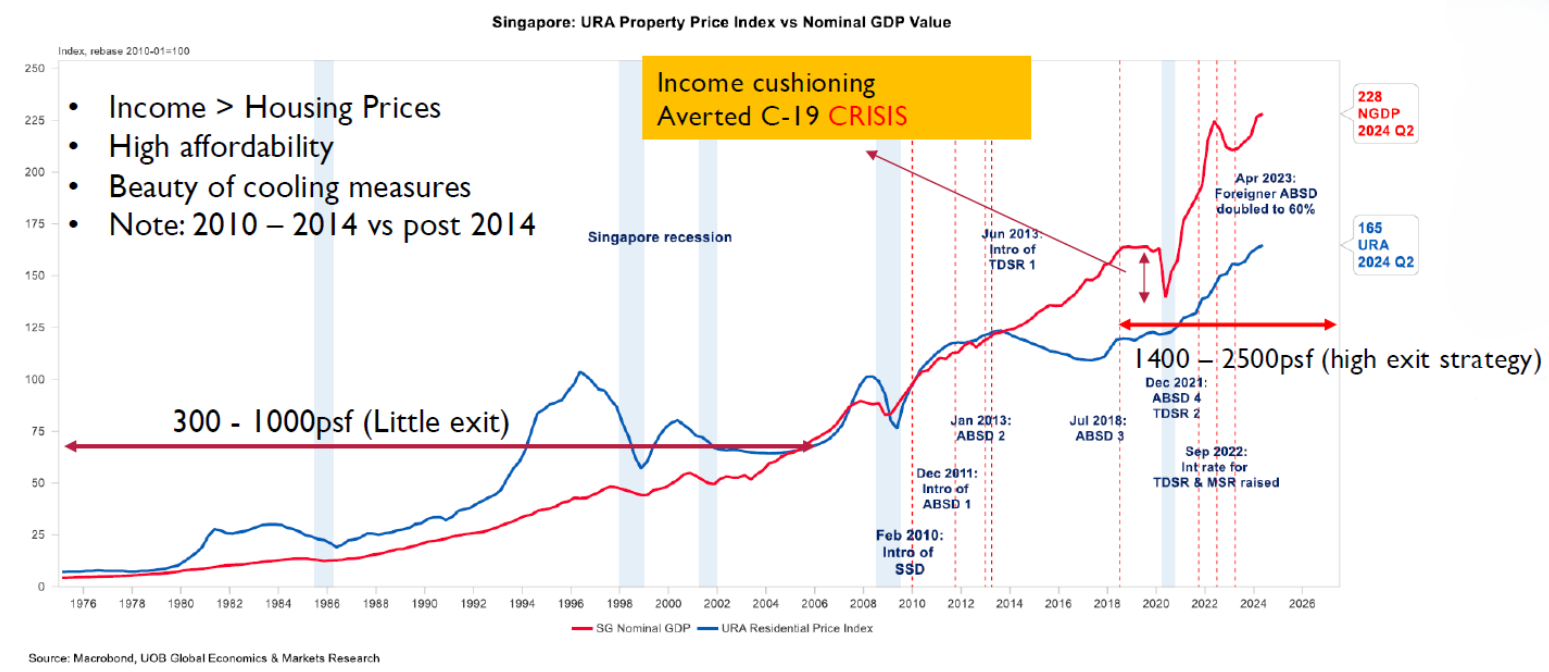

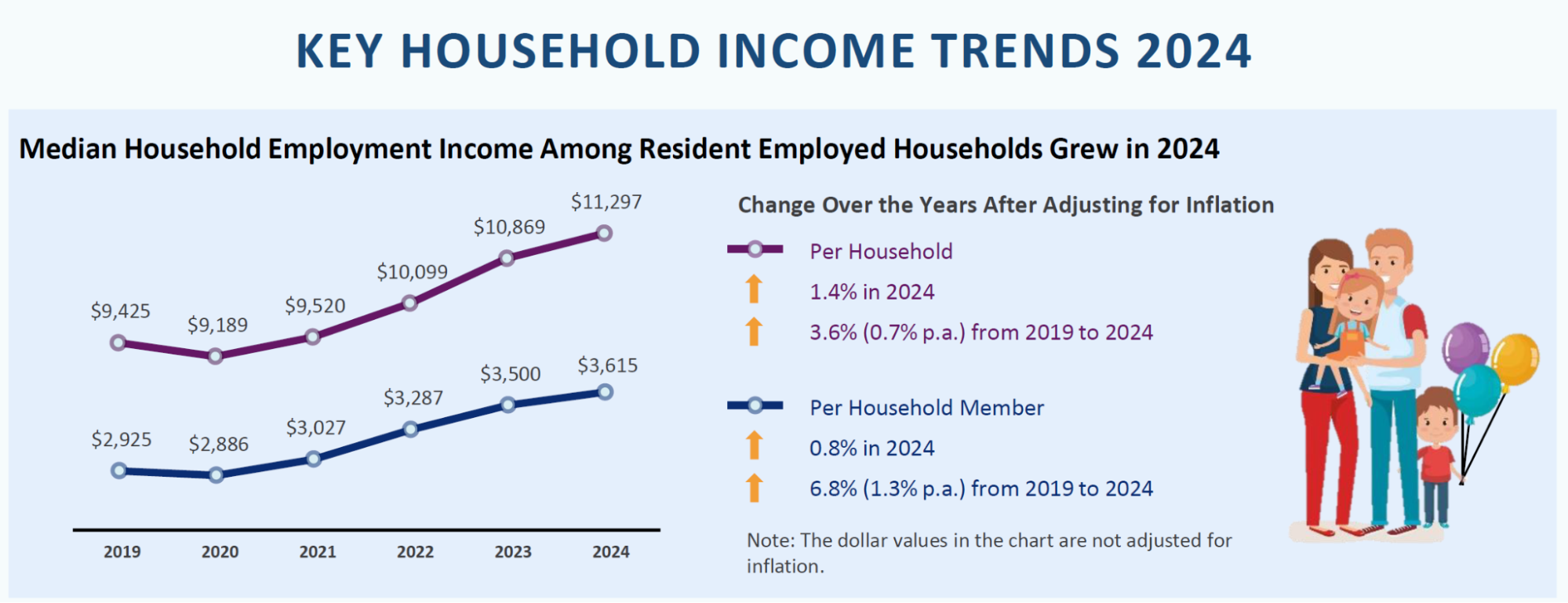

(This chart shows how Singapore’s nominal GDP (income) has consistently outpaced residential property prices since 2014 — highlighting the success of cooling measures in preserving housing affordability and creating a strong income cushion that averted a crisis during COVID-19.)

Singapore’s property market has always tracked one key tension: price vs. income.

But between 2014 and 2024, something significant happened.

That means income growth has nearly doubled price growth — a reflection of 14 rounds of cooling measures designed to prevent runaway speculation.

This affordability buffer is often overlooked in public discourse. While headlines warn of “record prices,” the deeper story is that Singaporeans today are better equipped than ever to afford them — especially in the CCR.

And that’s exactly what we’re seeing in the data.

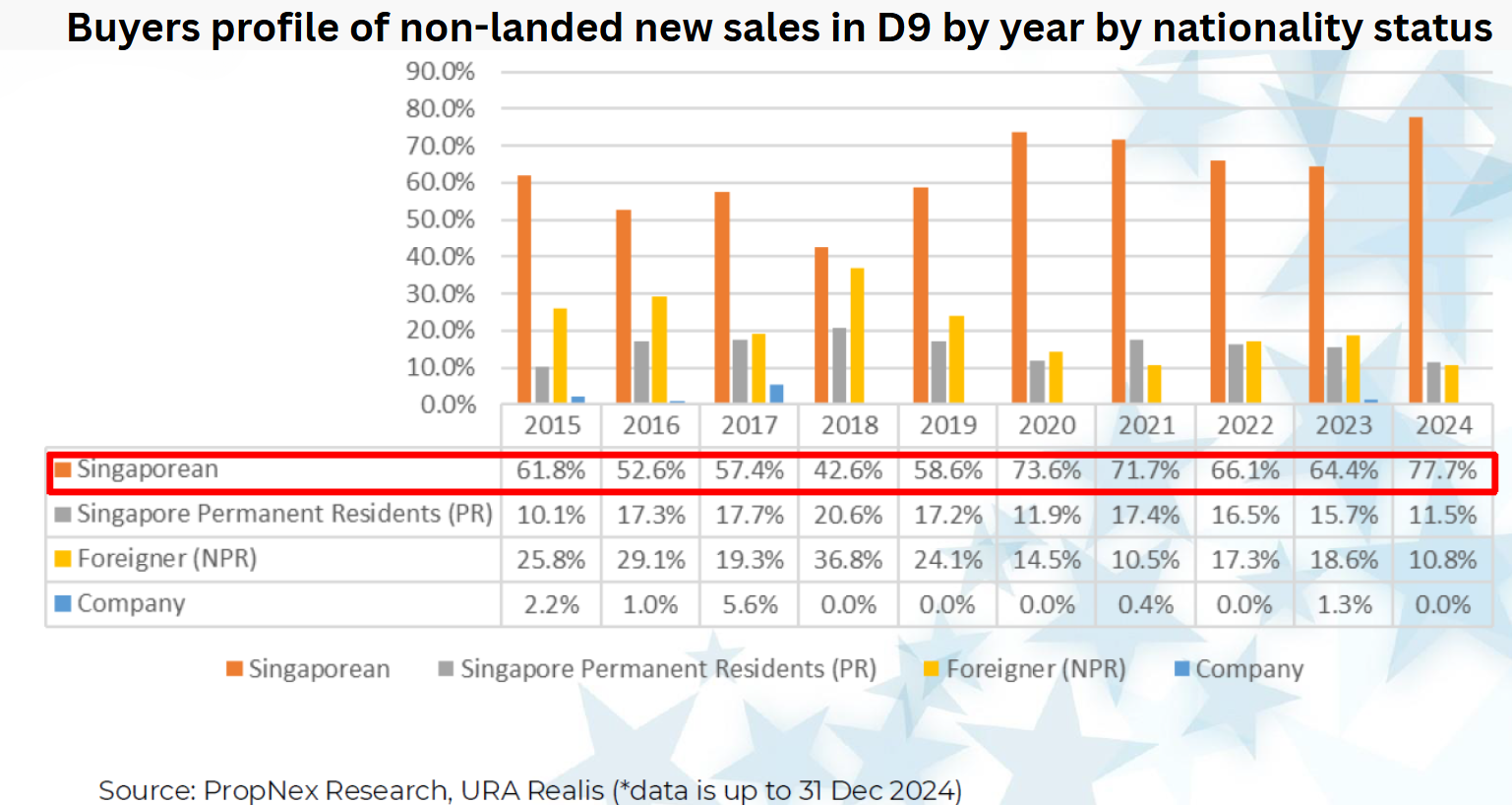

As of 2024, 77.7% of District 9 buyers are Singaporeans or PRs. In the wider CCR, the number reaches 90%.

That changes everything.

When locals buy, they buy to stay.

They’re not chasing quick flips or rental yield.

They have deeper financial buffers — and higher emotional stakes.

This localisation of CCR demand has two critical effects:

It also removes one of the biggest risks of CCR investment in the past: the unpredictability of foreign capital.

The CCR hasn’t just survived cooling measures — it has matured.

Today’s CCR is no longer driven by foreign inflows or trophy buying.

It’s supported by genuine local demand — backed by income growth, long-term plans, and higher thresholds for distress selling.

That’s why we didn’t see fire sales during COVID.

That’s why buyer activity remains steady even at higher interest rates.

And that’s why the CCR remains structurally more resilient — even if sentiment lags behind reality.

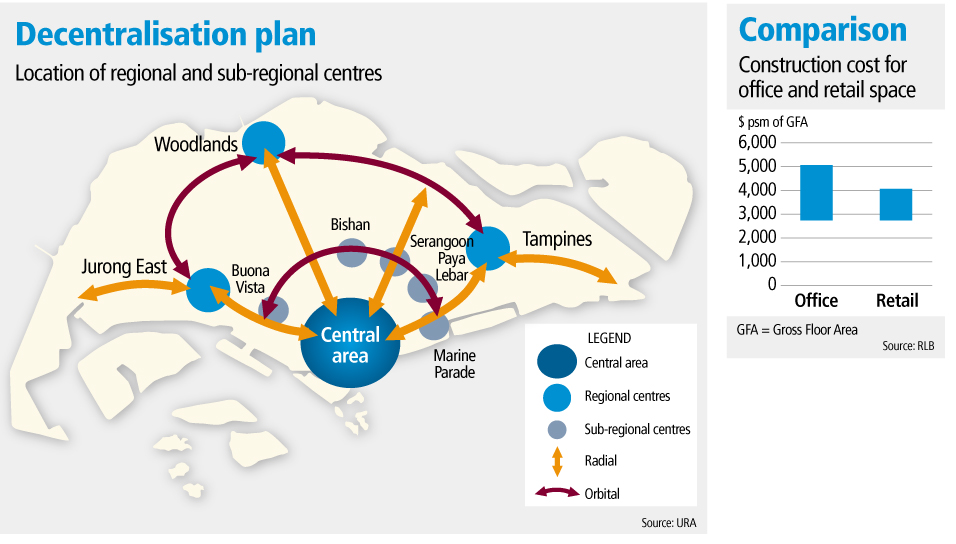

It’s tempting to blame URA’s decentralisation efforts for making the CCR irrelevant.

After all, if prime homes exist in Jurong, Tampines, or Paya Lebar… why pay extra for Orchard?

But that view is short-sighted.

Decentralisation didn’t kill the CCR — it added more steps to the upgrade ladder.

By improving infrastructure and amenities in the RCR and OCR, URA:

In doing so, it unintentionally made the CCR relatively affordable again.

Decentralisation didn’t kill the CCR — it recalibrated it.

We’re not witnessing a collapse. We’re seeing a realignment.

CCR’s current pricing is not a markdown. It’s a misread — based on outdated comparisons with a market that no longer exists.

You’re not buying the peak of the CCR.

You’re buying the bottom of a realignment curve.

Ask the average upgrader what comes to mind when they hear “CCR,” and the answers are predictable:

Orchard. Somerset. Dhoby Ghaut.

But those areas — while iconic — are clogged with dated freehold stock, aging infrastructure, and congested street layouts.

Transformation there is slow, because it depends heavily on en bloc cycles.

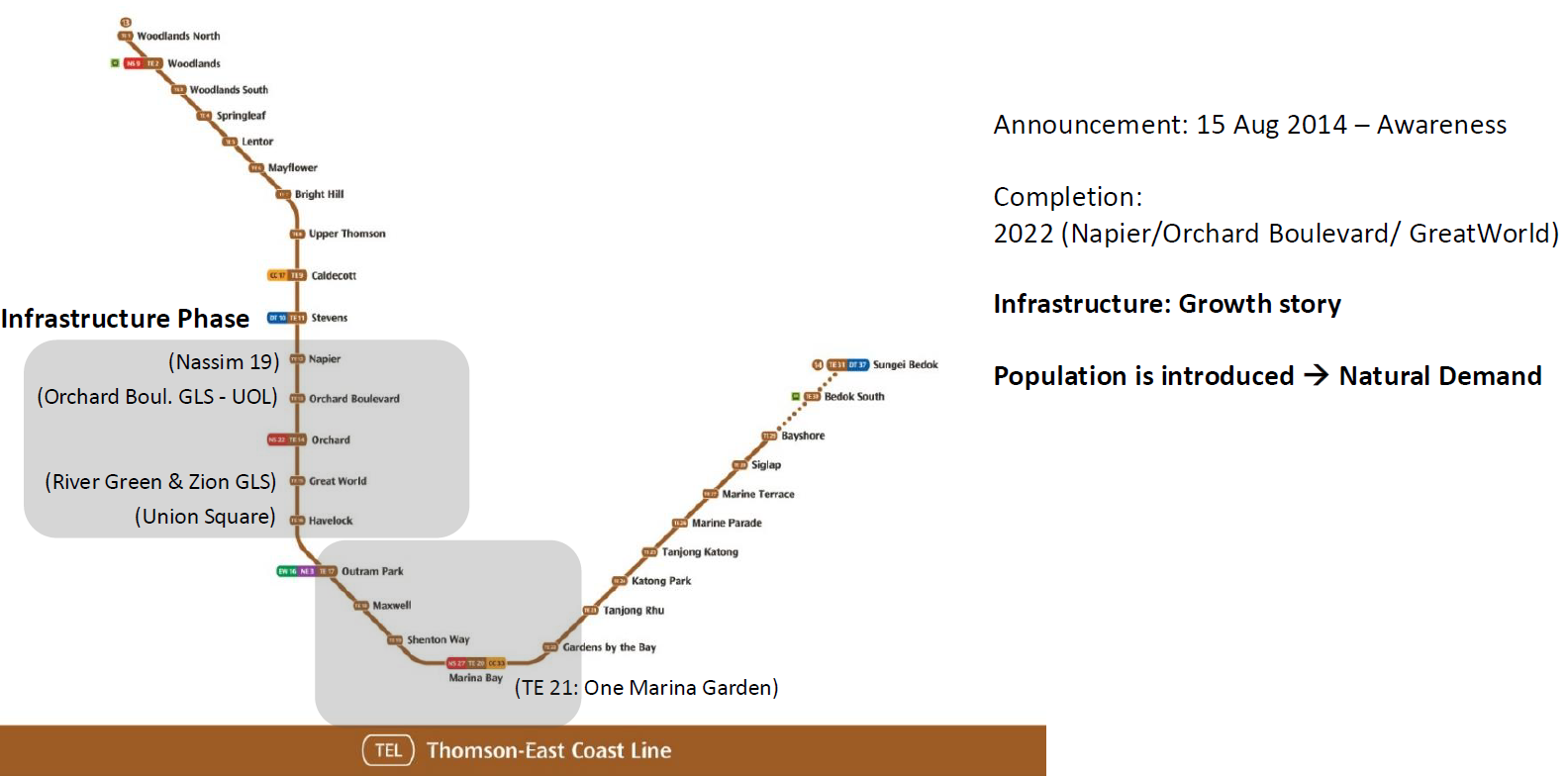

So URA and developers took a different path: they started building a new CCR.

With TEL stations (Napier, Great World, Orchard Boulevard) now live, and top developers shaping entire townships, we’re seeing the rebirth of CCR.

What sets these new CCR clusters apart?

Today’s buyers aren’t chasing districts. They’re choosing lifestyles.

And the new CCR nodes are quietly becoming the most livable — and undervalued — parts of the central region.

No thesis is complete without testing its blind spots.

Here’s where the cracks could appear — and why they may matter less than people think.

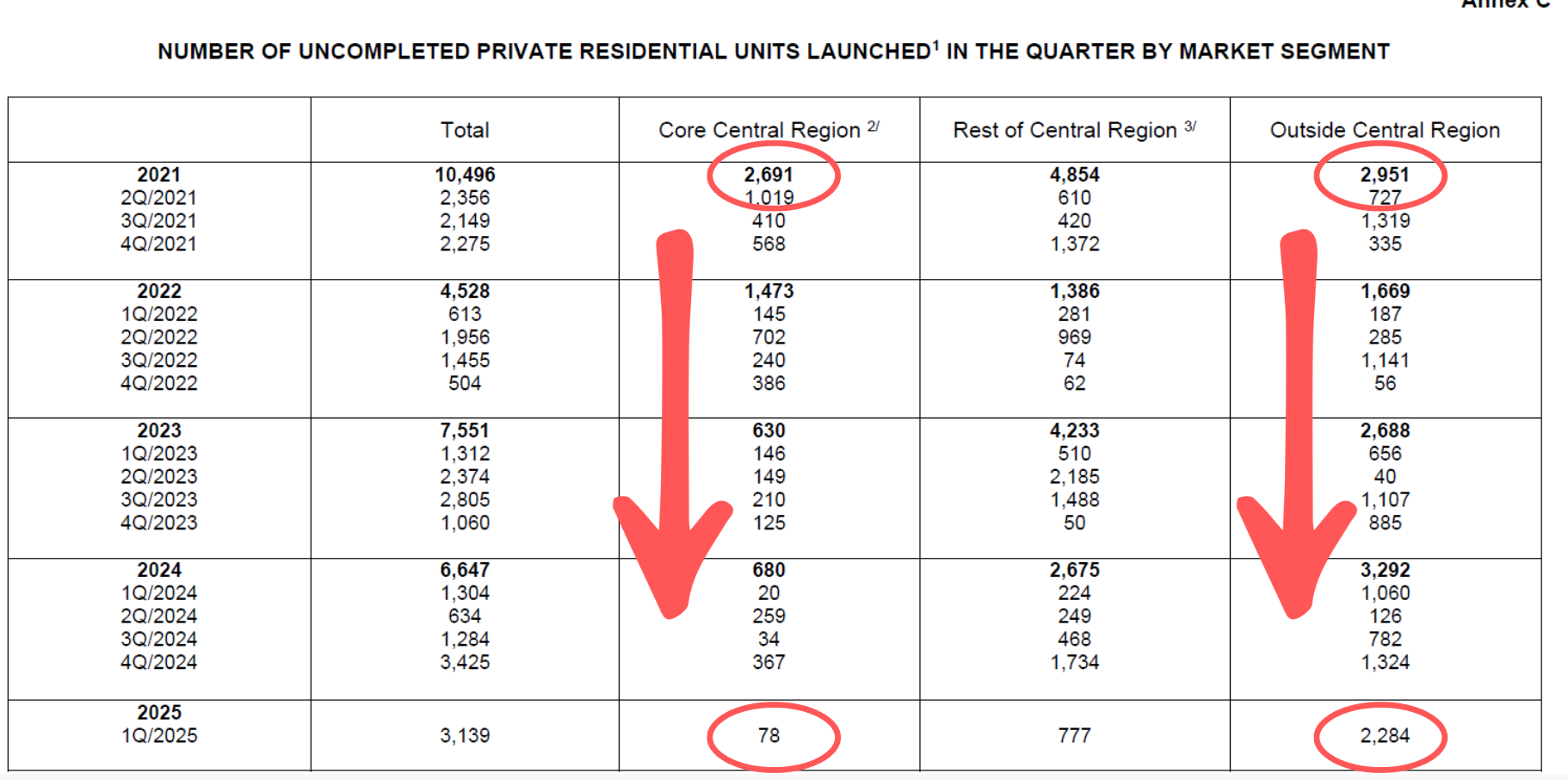

In Q1 2025, URA data shows a clear and growing disparity:

🟦 2,284 units launched in the OCR

🟥 Just 78 units launched in the CCR

And that’s not a one-off. Over the past four years, launch volumes have tilted heavily in one direction:

That means the volume imbalance isn’t just present — it’s structural. OCR has seen an outsized share of launches in recent years, especially in 2023–2025. As of Q1 2025, over 96% of all newly launched units came from the OCR, while the CCR accounted for just 3.3%.

If buying demand softens or interest rates remain elevated, the weight of unsold inventory will be felt more acutely in the OCR. Developers in this segment face higher land costs, tighter margins, and more direct competition.

The CCR, by contrast, has a more limited supply pipeline. With fewer units to clear and less launch activity, its exposure to price volatility may be lower — though not immune.

I’m not saying CCR can’t fall — I’m saying it’s more insulated than what people assume.

CCR’s greatest barrier has never been affordability.

It’s been perception.

For years, buyers didn’t avoid the CCR because they lacked the means — they avoided it because it didn’t feel justifiable.

The leap from OCR to CCR felt like crossing into a different financial universe. The numbers looked disconnected from reality.

But the numbers were never the real issue — belief was.

Now, the data tells a very different story:

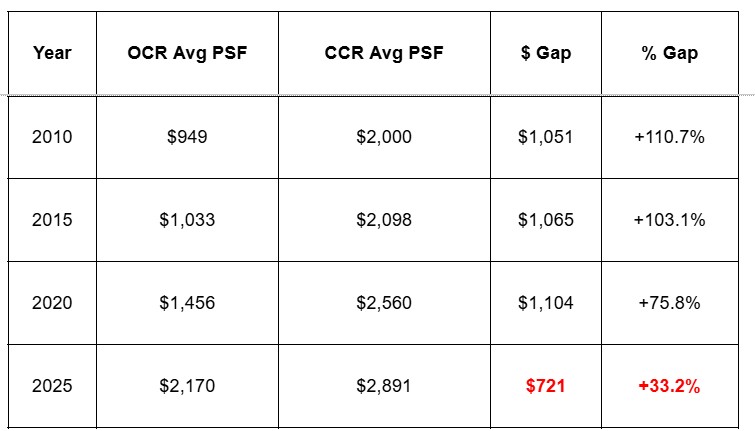

The price gap between CCR and OCR has collapsed — from over 100% in 2010 to just 33% today.

This isn’t just a number shift.

It’s a psychological unlock.

And this closing gap isn’t a fluke — it’s the result of two decades of decentralisation, income growth, and layout reform.

So the real question isn’t “Can I afford CCR?”

It’s “Why is it still being treated like a luxury tier… when it’s priced like a next-step upgrade?”

When belief lags behind data, smart money doesn’t wait.

And right now, the data is already there.

Could more cooling measures emerge?

Possibly — but unlikely, as long as CCR growth remains steady and demand stays locally anchored.

In recent years, policy has targeted mass-market overheating, not the core.

The government’s priority is to keep the upgrade ladder stable — and a healthy CCR is a part of that equation.

Singapore’s market doesn’t reward hesitation.

It rewards clarity — backed by numbers, timing, and product fit.

Today, most buyers still walk into CCR conversations with the old playbook:

“It’s too expensive. It’s for landlords. It’s not practical.”

But that playbook hasn’t been updated since before:

And yet, sentiment hasn’t caught up.

Most are still comparing old CCR to new OCR.

They haven’t realised it’s now new CCR vs old logic.

So here’s what I’ll say — not as a salesman, but as someone who’s walked hundreds of clients through this decision:

Then don’t dismiss CCR just because it hasn’t boomed yet.

The best deals rarely come with fanfare.

They come quietly, before consensus catches up.

Let’s talk. I’ll show you what others haven’t noticed — and what this window of mispricing is really offering.