Recently, I had a conversation with a friend that made me reflect deeply.

He reminded me why so many Singaporeans get stuck after buying their first home — and why others, quietly but steadily, keep progressing.

It’s not luck.

It’s not magic.

It’s a matter of perspective — and how you use four quiet forces working in the background.

Today, I want to share about the 4P Capital Building Concept — and how it can change your future, even if you’re starting small.

Most people only think about buying one property and staying there.

But those who manage to grow their property wealth understand there are four forces quietly working for them:

If you can get these four working for you, even a modest first step can snowball into serious capital over time.

Let’s dive in.

A good friend of mine is currently serving in the military.

He bought his Tampines North 5-room BTO a few years ago for less than $500K.

Today, it’s worth over $900K. We were chatting, and he was asking about buying Aurelle recently.

You might think, “Wah, confirm will upgrade already!”

But no — he has decided to stay put.

His reasoning?

“ After you deduct:

He shared that even those who “make” $300K–$400K on paper often only cash out less than $150K after everything.

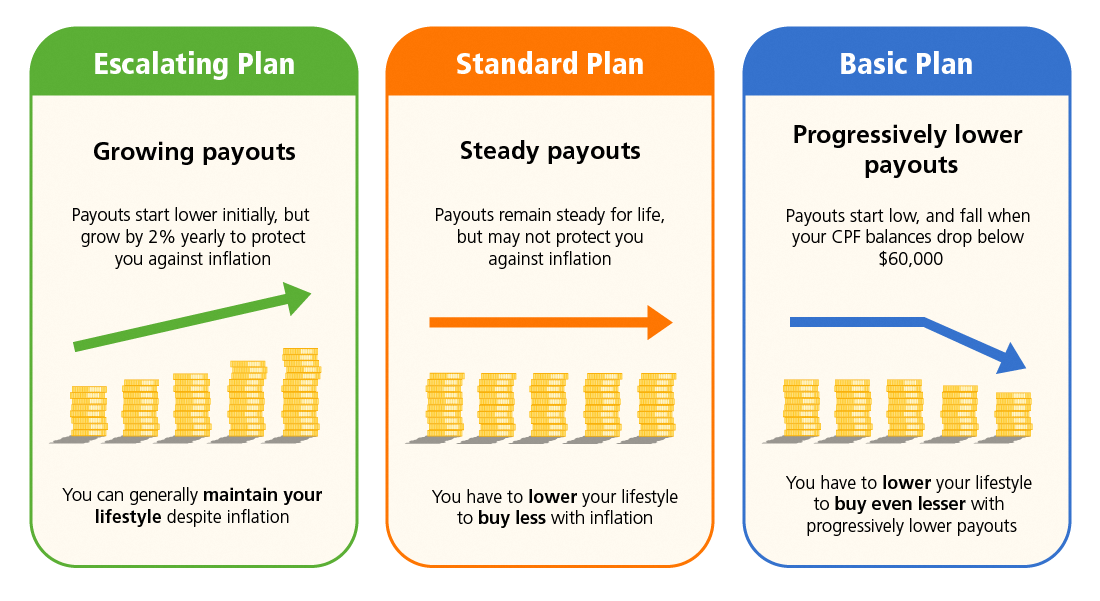

Instead of upgrading, he plans to deploy his CPF money into his Special Account — letting it grow at 4% compounded — aiming for a strong CPF Life payout.

As of today, at the age of 36, he and his wife have enough in their OA today to clear their entire HDB loan.

And honestly, it’s a smart and stable plan — if your priority is defense and stability.

But it’s very different from those who aim to actively grow capital through property.

In 2019, a former senior of mine from Geylang NPC (where I served my National Service) reached out to me after watching some of my property videos.

(Side note: I’ve always felt very blessed. Over the years, many brothers and seniors from the police force — who followed my journey since I was just 21 — have placed their trust in me.)

Back then, this young couple was earning about $8,000/month combined.

Buying a 4-bedroom condo felt like a distant dream.

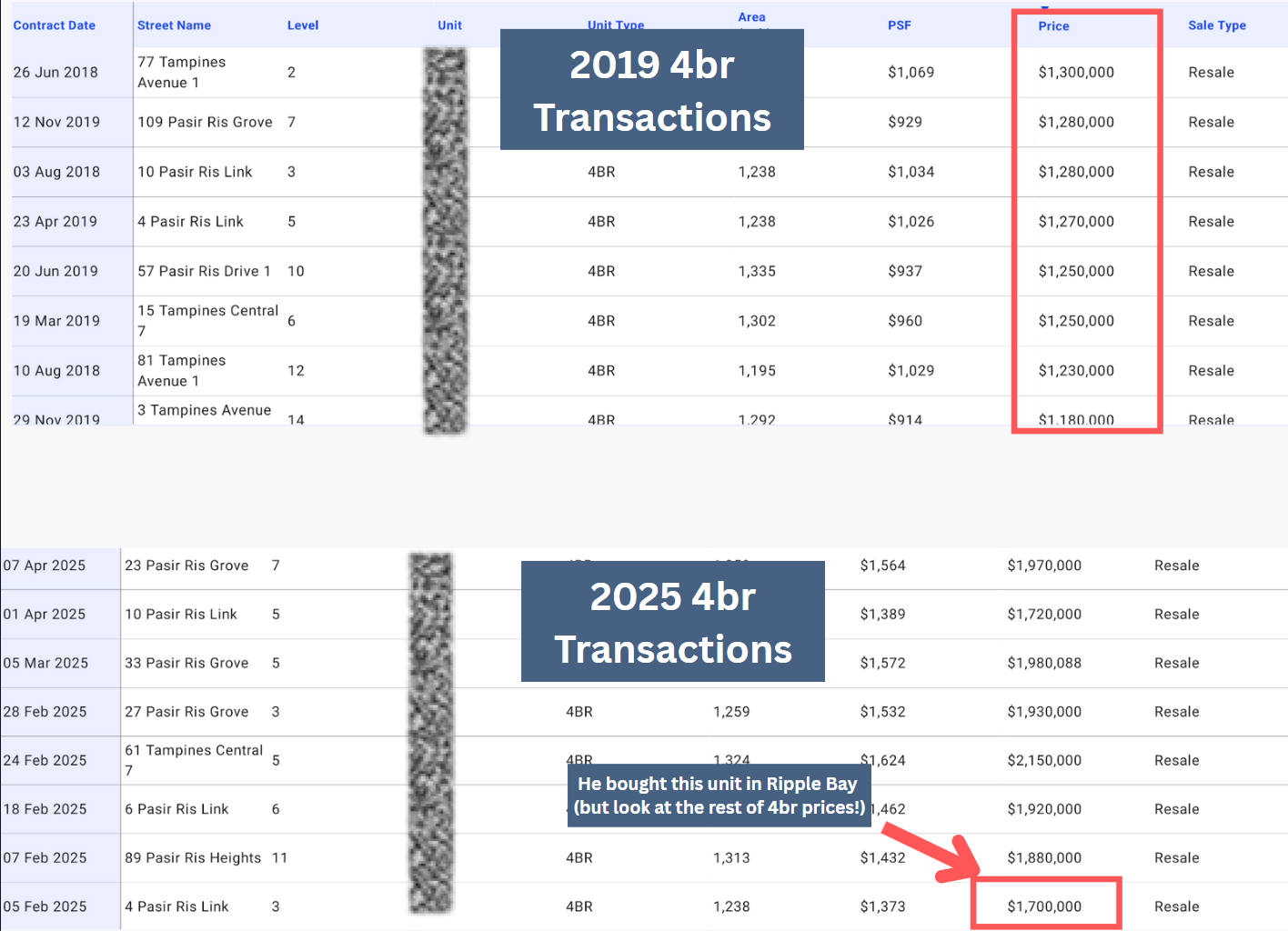

In fact, the same 4-bedder they eventually bought for $1.7M in 2025 was selling for just $1.25M in 2019.

Almost half a million dollars cheaper.

Yet they couldn’t buy it — because:

They simply weren’t ready yet.

Instead, I kick-started with what they could afford:

A 3-bedroom resale condo in Pasir Ris for $950K — their maximum safe budget.

It wasn’t glamorous.

But it was a solid first step.

Fast forward to 2024–2025:

(And importantly, they didn’t even need to touch their separate cash savings for the next step.)

Now, upgrading to the $1.7 million 4-bedder meant needing:

In total, about $485,000 upfront.

But here’s the important part:

Instead of just paying the minimum required downpayment,

they chose to deploy more capital into their new purchase.

They deposited more than necessary —

reducing their final loan to just above $1.1 million —

as part of their long-term strategy to increase their holding power.

This means:

It wasn’t just about upgrading.

It was about upgrading with strength.

Without that first stepping stone — the $950K 3-bedder —

they would never have been able to catch up with the market.

It wasn’t perfect timing.

It wasn’t luck.

It was capital building through action:

Because they moved carefully — and fortified their position each time —

they didn’t just chase bigger homes.

They built real security for the next stage of their life.

I’ve seen this pattern again and again over the years.

The ones who move early — even when it’s uncomfortable — get access to bigger options later.

And those who wait?

They watch the market move away from them…

and they end up paying tomorrow’s prices with yesterday’s savings.

By the time they realise it,

the gap is too wide to catch up.

The longer you wait, the more you are not just standing still —

you are quietly falling behind.

Let’s revisit the 4P concept — but this time, with real-world meaning behind each part:

When you stack these four forces,

you create momentum that opens bigger doors every few years.

If you:

You’ll wake up 5–7 years later, and realise:

Comfort feels nice short-term.

But comfort often costs capital long-term.

Here’s a realistic, achievable growth pathway:

| Stage | Starting Capital | Property Quantum | New Capital After Sale |

|---|---|---|---|

| Stage 1 | $250K–$350K | $900K–$1M condo | $500K–$600K |

| Stage 2 | $600K | $1.6M condo | $800K–$900K |

| Stage 3 | $900K | $2M–$2.5M bigger home or landed | $1.1M–$1.4M |

The key?

Start before you feel ready.

Grow as you go.

Let the 4Ps work quietly for you.

Before I end, I want to acknowledge that the “4P Capital Building Concept” was inspired by Matt Lam’s (my inspiring work boss!) original 4P framework. ( watch Video here : https://www.instagram.com/mattlamhy/reel/C3H-5WiSH8p/)

In Matt’s explanation, the 4Ps represent:

When these four forces come together, they can create a powerful roadmap to move you further ahead — even from humble beginnings.

If this article helped you think differently about your property journey, I’m really glad.

Because the truth is:

The best time to plan your next move is before you’re forced to.

Not when the market has already moved.

Not when financing rules change.

Not when opportunities dry up.

If you want someone to walk through the possibilities with you — calmly, clearly, and without pressure —

I’m always happy to chat.

You can WhatsApp me anytime at 9759 7125.

Sometimes one small conversation today…

can save you years of regret tomorrow.

Shall I do a video version of this topic?