Retirement is one of the biggest worries for most Singaporeans.

In 2023, ROSA’s research revealed that only 34% think their retirement preparedness is sufficient. With concerns about declining health, skyrocketing prices, and increasing healthcare costs, many voices doubt the adequacy of their retirement strategies.

As we offer perspective into solving this conundrum, we will delve into retirement strategies. Comparing CPF or housing, which is a better option for a safer retirement?

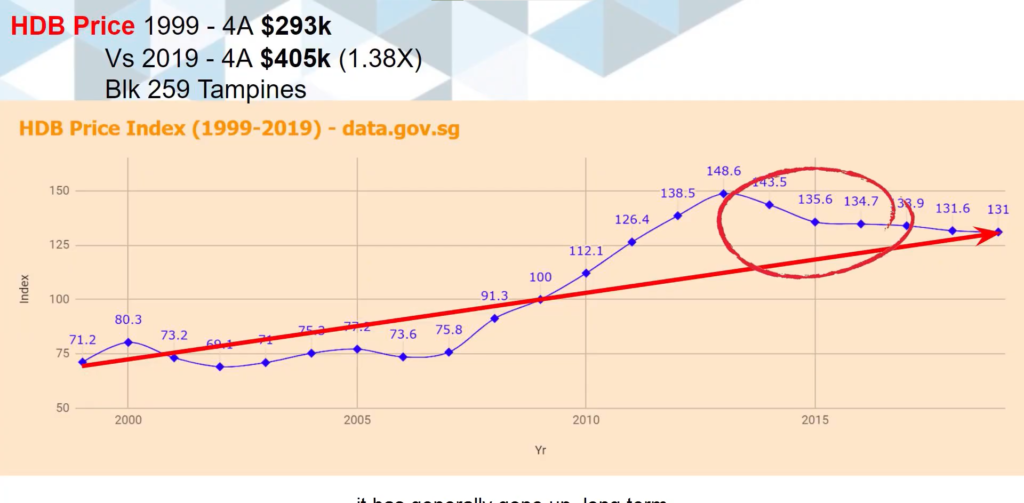

Property Prices on the Rise Since 1990

Properties are one of the most viable assets to leverage during retirement. But depending on your lifestyle goals, different properties may paint a different picture.

Suppose you can acquire any HDB, EC, or PTE at age 30; what will happen to you after having it fully paid at 60?

As no one knows how property prices will look in the coming years, analyzing past property transactions could give us an insight.

Between 1990 and 2019, property prices continued to soar.

To paint you a picture, let’s look at some of the stories of property owners who bought their homes in 1990

The first person bought a 3-room flat in Tampines for $55,000. Years after, in 2019, he saw the same property skyrocket six-fold to $340,000. In the same neighborhood, the second person bought a 4-room flat for $97,000 which jumped to $427,000 in 2019. The same happened for the third person who bought a 5-bedroom flat for $180,000. In 2019, the value of his property increased to $534,000.

Obviously, all the stories sound great, it’s not everyday that you will see property prices increase six-fold. But what really matters is the options they end with comes time to downgrade.

The first individual, who bought the 3-room flat, faces limited choices, ending up with only a 1-bedroom flat upon downsizing; 3rd person, however, would still end up in a 3-bedroom flat with $170,000 cash proceeds to spare for his savings.

CPF Retirement Sum Increase

Retirement planning is intricately linked with Central Provident Fund (CPF). Despite constant complaints regarding the continuous hike of the required retirement sum, these adjustments are necessary to keep up with inflation and the soaring living costs.

A concise timeline of CPF retirement sum increases reveals a steady growth rate since 2003. Initially $80,000 in 2003, it escalated to $181,000 in 2019, and $198,800 in 2023. Leaving us with an average inflation rate of 3%.

This sum is projected to go up to $228,200 come 2027, calculated at an inflation rate of 3.5%. This, of course, is still subject to change depending on Singapore’s financial landscape.

Balancing Retirement Needs

Singapore boasts the world’s longest life expectancy at 84 years. Which means our retirement plan needs to last longer.

Suppose you are living on a $2500 monthly budget until you are 60. To cover your expenses for 24 years until you’re 84, you must have a total of $720,000. But that is just for yourself. If you are married, this budget will double to 1.4 million.

One way you can contribute to preparing such a huge amount is by leveraging property assets. Say, if you have a 5-bedroom flat today, downgrading in the future can give a cash proceeds of $170,000. Although just a tiny part of your needed sum, it is substantial enough to fund your desired savings further.

The Ideal Retirement Plan

A secure retirement plan combines both CPF and housing.

Seeing how property values doubled over the years, it is a viable source of cash generation for retirees outside your CPF.

Think about it. If you have a fully paid property at age 60, depending on its type, it could yield significant returns once it is time to downsize. For a fully paid HDB worth $500,000 in 2019, you can project $150,000 in savings upon downsizing. For an EC worth $1 million, the savings could amount to $650,000; for a fully paid private property, that could yield $1.6 million.

When planning your retirement, consider how much you will get from a property in combination with your CPF balance.

Conclusion:

To have a secure retirement plan, balancing CPF and property is essential. Having a property is an excellent second source to fund your retirement outside of CPF, offering a holistic approach to a secure financial future.

But while having both is the ideal scenario, having a single retirement source would suffice in combination with sound financial management. Through meticulous planning and informed decision-making, you can confidently navigate the complexities of retirement.

Thinking of upgrading to a property? Consult with us. We are dedicated to match you with the best properties suited to your current and future needs.